I. Monetary Stability

The currency challenge ...

One of the main challenges and election promises of Javier Milei is to end inflation and dollarize the country.

- Milei inherited a 25.5% monthly (!) or more than 200% annual inflation rate. The country was heading toward hyperinflation.

- Milei received a country with across-the-board capital controls and an unsustainable official exchange rate: Milei started with a 200% gap between the official and market exchange rate, that is, the market exchange rate was twice the government rate.

- Milei is attempting to balance the federal budget (go to the Fiscal Monitor), because excessive government spending is the main culprit of inflation.

- Milei is cleansing the central bank's (BCRA) balance sheet in order to eventually dollarize the country and close the central bank.

The main goal of monetary policy is price stability. In this sense, we can distinguish between domestic price stability (related to inflation) and foreign price stability (related to the exchange rate). Inflation can be measured in various ways, the most common being the consumer price index (CPI).

Inflation

(Monthly) inflation rate

As a consequence of the high levels of inflation, it is customary in Argentina to report a monthly inflation rate instead of annual, which is more conventional. Milei's government achieved a large reduction in inflation, lowering a monthly 25% inflation rate to approximately 4%.

(Monthly) inflation expectations

Inflation expectations reflect the possible tendencies of future inflation rates and the confidence of the private sector in the Argentine fiscal and monetary policy. Lower inflation expectations suggest more confidence in positive future policy outcomes.

Breakdown of inflation

The inflation rate includes different types of prices: seasonal prices, core prices and government-controlled or regulated prices.

Seasonal prices

It is useful to distinguish between seasonal causes and non-seasonal causes, such as energy prices, of price increases.

Core prices

Core prices exclude seasonal elements, whereas seasonal prices are more volatile over the course of a year.

Government-controlled prices

Government-controlled or regulated prices should, perhaps, not even be called prices. However, as they are typically included in price indexes, they partly determine inflation rates. Therefore, it is useful to monitor their tendency separately.

Exchange rate

The other major goal of monetary policy stabilization is the exchange rate.

The exchange rate measures the price of one currency in terms of another and is an indicator of how cheap/expensive the prices of goods or investments abroad are compared to those domestically.

A sound currency is a stable currency.

Exchange rate gap

The exchange rate gap is the differential, in percentage terms, between the market exchange rate and the official (governmental) exchange rate.

Ideally, the exchange rate gap would be zero, as it implies the non-existence of an official exchange rate, and therefore, all currency exchanges would be made at market prices (with the consequent gain in economic efficiency).

Milei's short- or medium-term goal is to completely eliminate the exchange rate gap.

II. Causes of Monetary Stability

Causes of monetary stability

Our second group of indicators refers to the causes of monetary stability. Therefore, in the face of a sound monetary policy, we would expect these indicators to be the first to respond to policy changes, and only after a while (monetary policy delays) will measures of monetary stability such as inflation respond.

Quantity of money in Argentina: Monetary Base

The first series of indicators is linked to the quantitative theory of money. With a greater quantity of money, we would expect, under the auspices of this theory, that inflation would increase. The opposite would also be true. A drop in the pace of growth of the quantity of money would have the effect of generating disinflation (a decrease in the rate at which prices are rising).

The monetary base is the most restricted form of money, but it is the one that is closest related to monetary policy.

Quantity of money in Argentina: M2

M2 is a broader monetary aggregate and shows more accurately the money supply in the hands of the public, money that can exert upward pressure on prices.

M2 includes different types of deposits from commercial banks, which means that monetary policy can only have an indirect effect on M2.

Quality of money

The second series of indicators that cause monetary stability are linked to the qualitative theory.

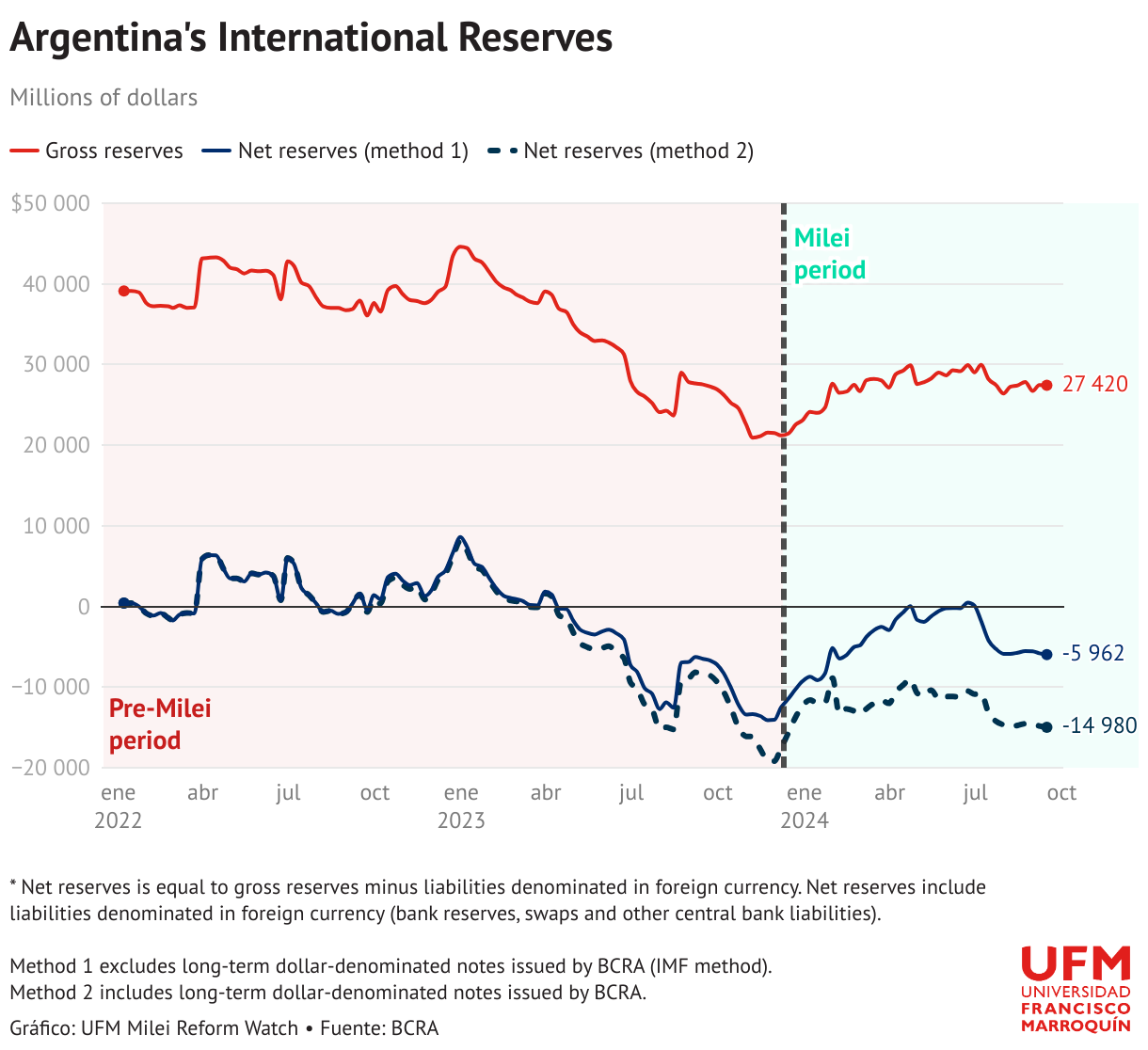

The quality of money has several dimensions. The first one we will study is its backing. In economies with non-central currencies, the amount of international reserves is crucial when it comes to supporting the national currency.

The principle is simple: in case of overselling of the currency, the monetary authority can withdraw the excess supply by selling off international monetary assets.

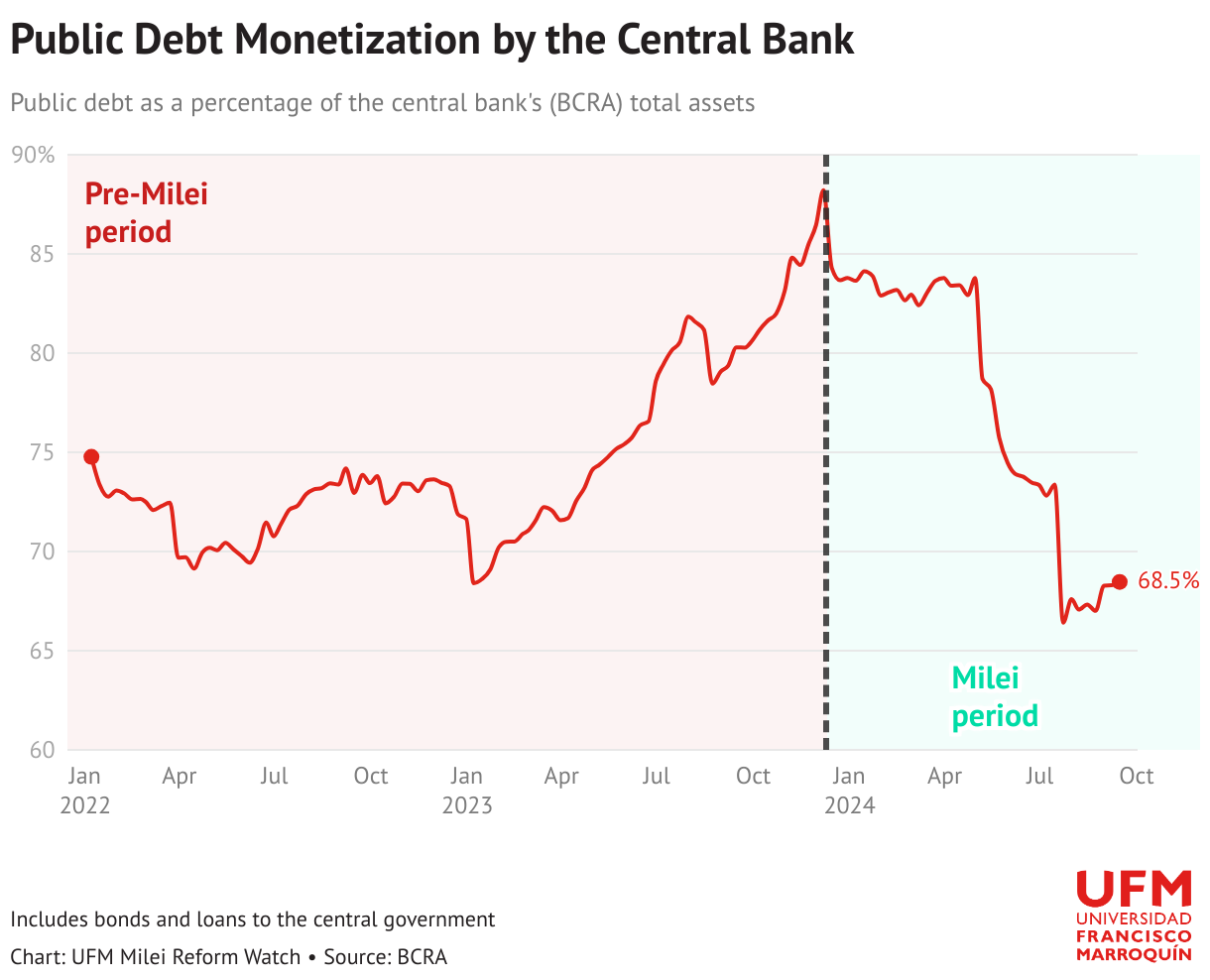

Public debt monetization

As a rule of thumb, monetary backing since the 20th century largely consisted of public debt. An excessive amount of public debt, along with its monetization by the central bank, is the main cause of high inflation over the last century in a variety of countries.

The monetization of public debt is one of the main reasons why inflation makes its appearance. When the demand for public debt is concentrated in the hands of the central bank, inflation tends to skyrocket.

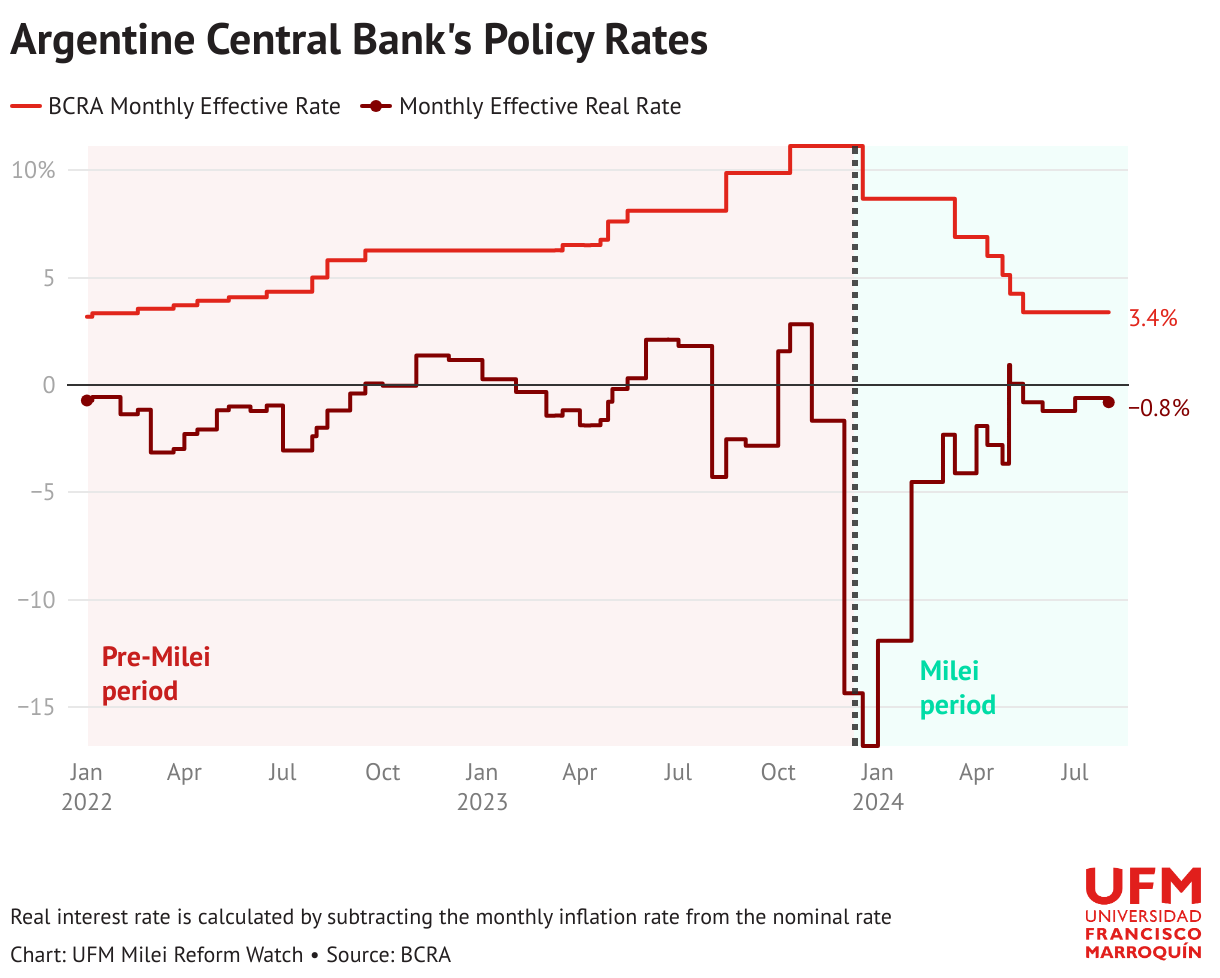

BCRA policy rate

The monetary policy interest rate is the central bank's target (short-term) interest rate that it seeks to fix.

In this context, a positive real interest rate suggests an increase in purchasing power for those who have very short-term investments in the money market.

Similarly, a negative real interest rate indicates a loss of purchasing power, because inflation is higher than the nominal interest rate paid in the short-term money market by the central bank.

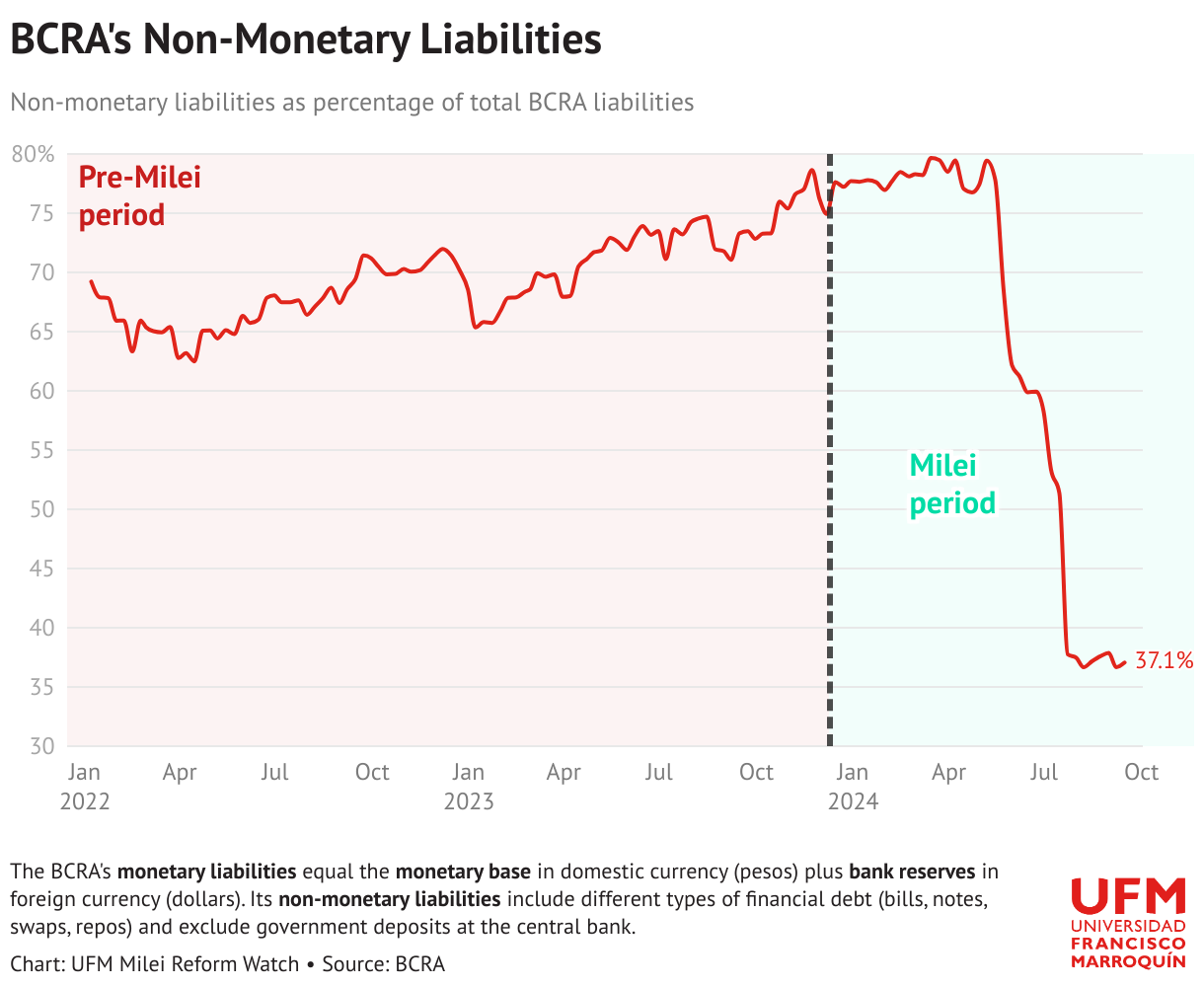

Non-monetary liabilities of the BCRA

The non-monetary financial liabilities of the Argentina central bank (BCRA) represent a way to approximate a future potential monetization of BCRA commitments and entail a postponement (not a solution) to Argentina's monetary problems.